Categories

The Laws of Supply and Demand: The Only Constant in 2020

In 2020 we saw one thing finally prove true within the Market Research industry – the laws of supply and demand.

When authoring these guest blogs I always struggle to come up with a topic that is interesting yet doesn’t espouse self-serving business jargon. This time around, the topic was so obvious, transformative, and important that I couldn’t wait to write it. I want to talk about what we’re seeing from a supply/demand perspective and how I see this playing out the balance of 2020 and beyond. Some of the preconceived notions are going to be challenged, however, the goal is for everyone to prepare for the next calendar year in a way that is more aligned with the direction of the industry.

Before we jump ahead, I should introduce myself and the company. I’m Michael McCrary and I founded PureSpectrum in 2016 after spending nearly thirteen years in the online sampling sector of the insights industry. I’ve had the privilege of working for innovative technology companies throughout my career and have witnessed both slow evolution and rapid changes take place in our industry. To some, I’ve made some pretty bold predictions over the years and am always careful to caveat that although I have a strong belief in what will transpire, I’m less sure of when.

What Will Happen

I’ve been predicting for years that pricing would stabilize and ultimately obey the economic laws of supply and demand. How often have you had a sales rep tell you that if you buy more they’ll reduce the CPI (cost per interview)? Even more common, a sales rep will just lower their price in order to win the business regardless of the order size. This belief and behavior have led to lower CPI’s pretty much ever since I was selling sample in 2003 for Greenfield Online.

Over the past 17 years, I’ve seen the demand for online survey participants grow while prices have gone down in almost every category. As long as the availability of supply (survey participants) is growing at a higher rate than the demand this is perfectly rational. Although I can’t provide proof, my sense is that the available pool of survey participants has not grown at the same rate of demand over the same time. Rather, new companies have entered the industry driving competition and innovation up while driving prices down.

Enter the present day, where the delivery of survey starts is performance-driven based on a myriad of factors including price, conversion, survey length, and other factors. It has taken years for the online sampling ecosystem to refine and adapt to this model and there’s still a long way to go. If you’re a research agency or corporate researcher this is probably starting to impact your business in a very direct way, however, the underlying reasons might not be making its way to you. Right now you may be experiencing delivery issues on some or all of your surveys, many of which, you’ve never experienced before. Why is this happening? It’s coming down to a few factors. For years I’ve made the same prediction that pricing would behave rationally, and every year, I was wrong. However, this year has brought about a material transformation that would have otherwise taken longer to gain traction.

Factor #1 – Supply and demand simultaneously and rapidly contracted

The Covid-19 pandemic forced every company in the world to make immediate and harsh decisions. Faced with unprecedented uncertainty, two competing factors came head to head. Buyers sought to drive down pricing to preserve margins while Suppliers drastically cut recruitment budgets to accomplish the same business objectives. Both parties acted rationally.

Factor #2 – Demand recovered faster than Supply

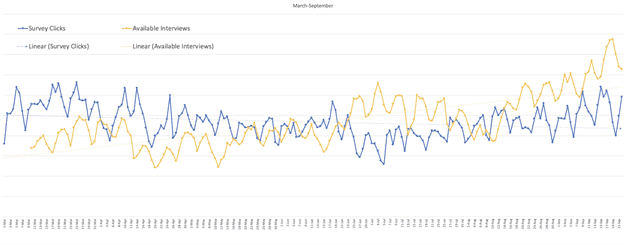

Between April 8th and June 20th, we witnessed a shallow U-Shaped reduction in demand that hit the low point on May 10th. From May 10th onward, we experienced a steady increase in available interviews that reached pre-lockdown levels by the first week of June and sustained growth above pre-lockdown levels by July.

At this point in early July, we saw something we’ve rarely witnessed, which was that the number of available interviews (Demand) was higher than the volume of the daily survey starts, or “clicks” (Supply). This has happened on occasion before, but it became a persistent trend where now the opposite occurrence (clicks are higher than available surveys) is a periodic occurrence.

Source: PureSpectrum Platform

Factor #3 – Supply has been slower to rebound

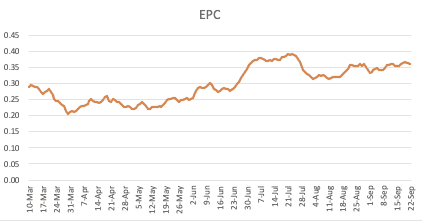

Compared to the relatively short-lived reduction in demand accompanied by lower price offers in April and May, the availability of survey starts has taken much longer to recover to pre-lockdown levels. During the same time period, we’ve also observed a dramatic increase in Earnings Per Click (EPC) on our platform.

Factor #4 – Surveys are competing for delivery

EPC is one of the most important factors in the delivery of survey participants. It’s the most reliable metric when determining the relative performance of one survey compared to all others. EPC is a simple calculation that takes the total amount of revenue generated (CPI X N) and divides it by the total amount of survey starts.

For example, Survey A and Survey B are competing for delivery.

| Survey A: | Survey B: |

| (n=100 x $5 CPI = total revenue) $500 = $0.50 EPC | (n=100 x $10 CPI = total revenue) $1,000 = $0.33 EPC |

| (Individuals needed to start the survey) = 1,000 | (Individuals needed to start the survey) = 3,000 |

Even though Survey B has double the total revenue, it’s EPC is less attractive than Survey A. Generally speaking, Survey A will not win all of the survey starts to the absolute detriment of Survey B, but it will receive priority delivery.

Source: PureSpectrum Platform

All of these factors have driven suppliers to expedite and prioritize yield management to ensure they are making the best and most profitable choices for delivery that favor the highest quality surveys.

As we all continue to manage through the murky waters ahead I’m cautiously optimistic that the economic laws that were thrust into action this year will continue. As an industry, we’ll transition from imperfect and irrational pricing and delivery and will ultimately enjoy the benefits or a more predictable and rational supply and demand relationship.

Photo by Ramiro Mendes on Unsplash

Comments

Comments are moderated to ensure respect towards the author and to prevent spam or self-promotion. Your comment may be edited, rejected, or approved based on these criteria. By commenting, you accept these terms and take responsibility for your contributions.

Disclaimer

The views, opinions, data, and methodologies expressed above are those of the contributor(s) and do not necessarily reflect or represent the official policies, positions, or beliefs of Greenbook.

More from Michael McCrary

Partner Content

The Five Eras of Online Sampling: An Industry Perspective

A 20-year industry veteran reflects on the key eras that reshaped market research, from shifting strategies to evolving KPIs.

Sign Up for

Updates

Get content that matters, written by top insights industry experts, delivered right to your inbox.